1 Dividend-Paying Dow Jones Stock to Buy in August

Key Points

Honeywell is getting closer to spinning off the first of three stand-alone companies.

The company’s full-year guidance showcases solid growth and tariff resilience.

Its stock is an excellent value for those who believe the split will unlock advantages.

With just 30 components, the Dow Jones Industrial Average isn't as representative of the broader market as the S&P 500 or Nasdaq Composite. But it's still an excellent resource for finding high-quality, industry-leading companies, many of which pay dividends.

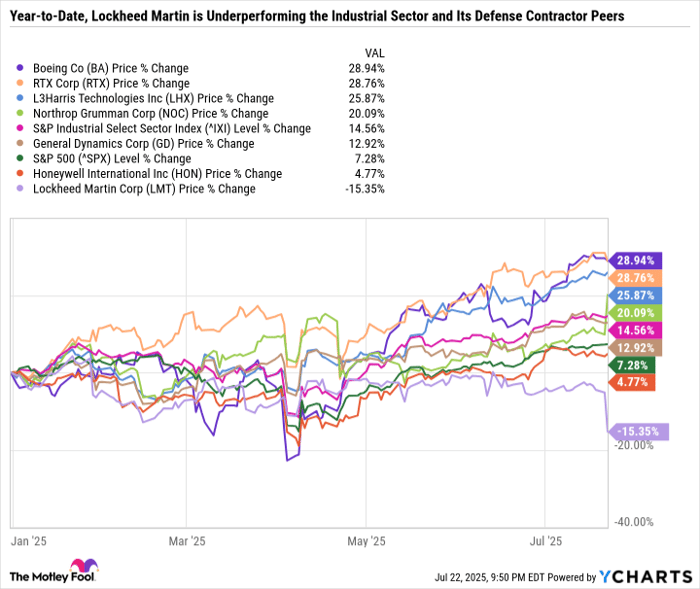

After nearly making an all-time high in July, Dow Jones component Honeywell International (NASDAQ: HON) is down 9.8% in the past month. The sell-off may come as a surprise, given that Honeywell delivered a great quarter, raised its guidance, and is producing high operating margins across its business segments.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Learn More »

Here's why the dividend stock is a great buy in August.

Image source: Getty Images.

Honeywell's conglomerate days are rightfully coming to a close

Shortly after becoming CEO in June 2023, Vimal Kapur launched a comprehensive portfolio review of Honeywell's businesses to try to give the once thriving industrial conglomerate a jolt. The company had been languishing, failing to capitalize on its three highest-conviction megatrends: automation, the future of aviation, and the energy transition.

Kapur and his team concluded that the best way to unlock value for shareholders was to split the company into three separate publicly traded businesses: Honeywell Automation, Honeywell Aerospace, and Solstice Advanced Materials. In July, Honeywell said it is on track to spin off Solstice Advanced Materials for the fourth quarter of 2025 and the other two companies in the second half of 2026.

The conglomerate structure isn't inherently bad. In fact, it can work well when it provides diversification and resources to help each business segment perform.

For example, Berkshire Hathaway owns insurance businesses; retail, service, and manufacturing companies; the BNSF railroad; the utility and energy infrastructure company Berkshire Hathaway Energy, and more. By owning quality businesses across various industries, Berkshire accesses different growth opportunities and end markets. And by not overly managing its businesses and having a leadership structure with very little red tape, it can avoid many of the downsides of a conglomerate.

Honeywell's decision to split into three companies is a way of admitting that being a big and bulky company with a lot of moving parts had become a net negative. And there's reason to believe each business can perform better as a stand-alone company.

But with roughly a year to go until the full separation is complete, Honeywell investors are caught in no-man's-land. The stock is down 8.3% since it published a news release on Dec. 16, 2024, announcing the decision to split into three companies.

Honeywell has a compelling valuation and quality dividend

Buying the stock now is based on the belief that the company is a good value and will be an even better one once it splits into three companies.

Honeywell reported 8% sales growth and exceeded the high end of its prior guidance in adjusted earnings per share (EPS) with a 10% increase. Its updated 2025 guidance calls for $40.8 billion to $41.3 billion in revenue, $10.45 to $10.65 in adjusted EPS, and $5.4 billion to $5.8 billion in free cash flow (FCF) -- or $8.43 to $9.05 in FCF per share. On its second-quarter 2025 earnings call, management said that it is committed to offsetting tariff impacts with productivity, pricing, and alternative sourcing.

Based on the stock price at the time of this writing of $216.31 per share, investors are paying just 20.5 times the midpoint of adjusted 2025 earnings and 24.7 times FCF. That's a steep discount to Honeywell's five-year median price-to-earnings ratio (P/E) of 25.5 and price-to-FCF of 29.5, and a good value compared to its 10-year median P/E of 23.6 and 24.5 price-to-FCF.

Or put another way, Honeywell is already an attractive valuation. If the split is a success and unlocks value, it will look like a steal at these levels in hindsight.

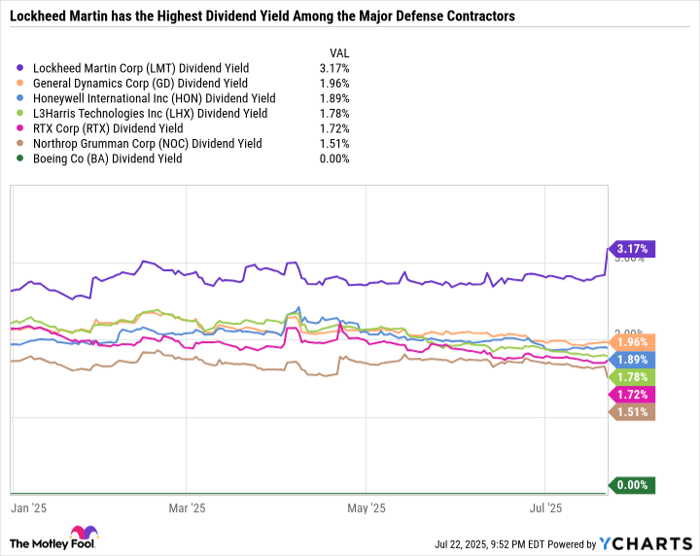

The company has a 14-year streak of boosting its dividend, which yields 2.1% at the time of this writing. It remains to be seen what the dividend will look like post-split, but Honeywell has the FCF needed to support future dividend raises: The midpoint of its 2025 projected FCF per share is nearly double its $4.52 its annual payout.

Honeywell is a buy before its breakup

The decision to split into three companies is the right move for investors, and the stock is a good value right now, making it a strong buy. Given how different aerospace is from industrial automation and sustainable materials, some investors may prefer to wait until post-breakup to invest in the business segment that is most appealing to them.

However, it's worth noting that the valuations of each stand-alone company could vary based on their growth. For example, Honeywell Automation's potential in artificial intelligence may lead this segment to fetch a higher valuation than the aerospace business, where even industry leaders tend to command value stock P/E ratios.

All told, investors who wouldn't mind owning shares in all three stand-alone companies may want to consider buying Honeywell now before the breakup.

Should you invest $1,000 in Honeywell International right now?

Before you buy stock in Honeywell International, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Honeywell International wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $660,783!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,122,682!*

Now, it’s worth noting Stock Advisor’s total average return is 1,069% — a market-crushing outperformance compared to 184% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of August 13, 2025

Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool has a disclosure policy.